No products in the cart.

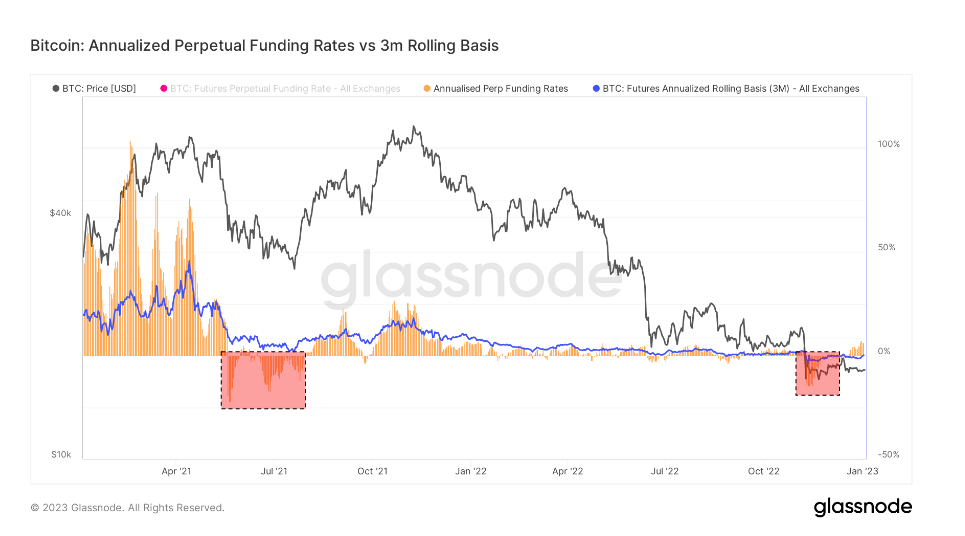

Among all cryptocurrency derivative products, perpetual futures have emerged as the preferred vehicle for market speculation. Bitcoin traders en masse use this tool to hedge risk and earn funding rate premiums.

Sometimes referred to as perpetual futures or perpetual swaps, these are futures contracts that do not expire. A person holding a perpetual contract can buy or sell the underlying asset at an unspecified time in the future. The price of the contract remains the same as the spot rate of the underlying asset on the contract start date.

To push the price of the contract closer to the spot price over time, exchanges implement a mechanism called crypto funding rates. A funding rate is a small percentage of the value of a position that must be paid or received from a counterparty on a regular basis (usually every few hours).

A positive funding rate indicates that the perpetual contract price is higher than the spot rate, indicating high demand. When demand is high, the buy contract (long) pays a funding fee to the sell contract (short), incentivizing the opposite position and pushing the contract price closer to the spot rate.

If the funding rate is negative, the sell contract will pay the funding fee to the long contract, bringing the contract’s price closer to the spot rate again.

Given the size of both the maturity and perpetual futures markets, comparing the two can indicate broader market sentiment about future price movements.

Bitcoin’s annualized 3-month futures basis compares the annualized rate of return available in cash and carry trades between 3-month futures and perpetual funding rates.

CryptoSlate’s analysis of this metric shows that the perpetual futures base is significantly more volatile than the expired futures base. The discrepancy between the two is the result of increased demand for leverage in the market. Traders appear to be looking for instruments that more closely track spot market price indices, and perpetual futures fit their needs perfectly.

Periods in which the perpetual futures basis trades lower than the 3-month futures basis have historically followed sharp price declines. The perpetual futures base often declines after major risk aversion events such as bull market corrections or prolonged bearish slumps.

On the other hand, perpetual futures-based contracts are trading higher than 3-month futures-based contracts, indicating a strong demand for leverage in the market. This causes an oversupply of sell-side contracts, leading to price declines as traders act quickly to bring down high funding rates.

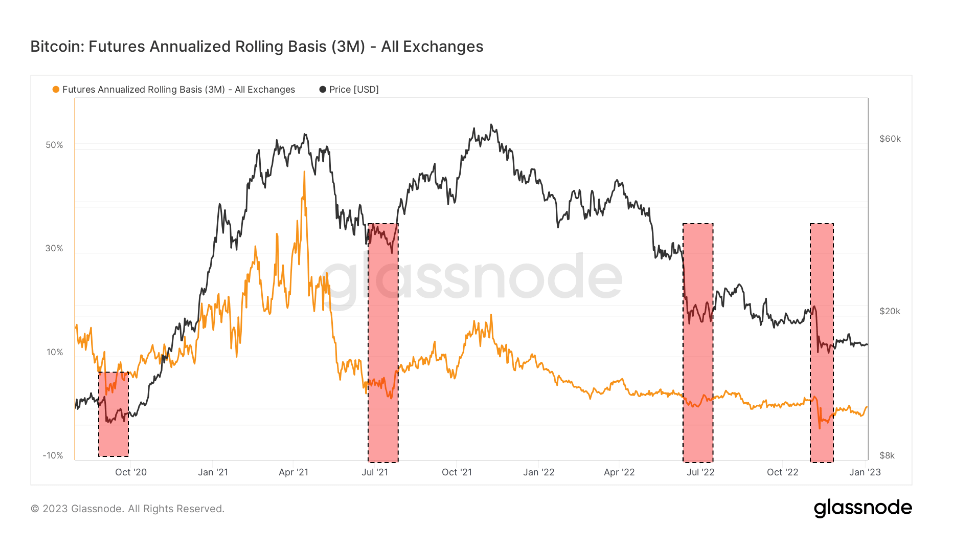

Looking at the chart above, we can see that both bitcoin expiring futures and perpetual swaps were trading in a state of backdation during the FTX collapse.

Backwardation is when the price of a futures contract is lower than the spot price of the underlying asset. Occurs when the demand for assets is higher than the demand for contracts maturing in the next few months.

As such, backwardation is a very rare sight in the derivatives market. During the FTX collapse, expiring futures were trading at -0.3% on an annual basis, while perpetual swaps were trading at -2.5% on an annual basis.

Similar periods of backwardation were only seen in September 2020, the summer of 2021 following the Chinese mining ban, and July 2020. During all these periods of backwardation, the market was hedged downwards and braced for further recession.

However, each period of backwardation was followed by an increase in price. The price increase he started in October 2020 and peaked in April 2021. It spent July 2021 in the red before continuing its upward trend until December 2021. Terra’s collapse in June 2022 saw an uptick in late summer that lasted until the end. of September.

The vertical price drop triggered by the FTX crash has resulted in backwardation that is eerily similar to previously recorded periods. You may see positive price action.

At the time of press, Bitcoin ranks first in terms of market capitalization, and the price of BTC is Up 1.06% Within the last 24 hours. The market capitalization of BTC is $325.89 billion 24 hours trading volume $12.84 billion. Learn more >

At the time of press, the global cryptocurrency market is valued at $823.22 billion at the 24-hour volume of $26.36 billionBitcoin dominance is now 39.59%. Learn more >