No products in the cart.

We are approaching the 14th anniversary of the global financial crisis of 2008 and are about to enter a new debt cycle that could reset the market. To survive future crises, we need a deep understanding of how all past debt crises worked and why they happened.

Ray Dalio, founder and chairman of Bridgewater Associates, was the first to put forth his theory of the typical mega-debt cycle. Dalio divides these into short and long cycles, the short cycle he lasts 5-7 years and the long cycle about 75 years.

These archetypes have formed the foundation of Bridgewater’s investment strategy and have served as lifeboats that have enabled hedge funds to weather the economic turmoil of the past three decades.

Looking at the current market through this lens, we see that we are nearing the end of the cycle that began with the signing of the Bretton Woods Accords in 1944. The Bretton Woods system effectively brought about what could be called a world order for the US dollar which lasted even after the gold standard was abandoned in 1971.

In a debt cycle, the lack of credit determines where the money goes. When credit is plentiful and money is flowing into the economy, people invest in scarce assets such as gold and real estate. When credit is scarce and the economy is short of money, people turn to cash and scarce assets are devalued.

Since 2008, interest rates have been incredibly low or near zero, dramatically increasing credit and money in the economy. The decline has significantly increased the value of scarce assets such as gold and real estate, as well as speculative investments such as stocks.

The most extreme example of this trend can be found in the United States, the world’s largest market-driven economy. However, the trend has pushed the US debt-to-GDP ratio above 100% and made the economy highly sensitive to interest rate movements.

Historically, liquidity crises occurred whenever the market saw significant movements in interest rates. Markets may be gearing up for an unprecedented liquidity crisis as the US Federal Reserve (Fed) is expected to continue to raise interest rates aggressively until next spring.

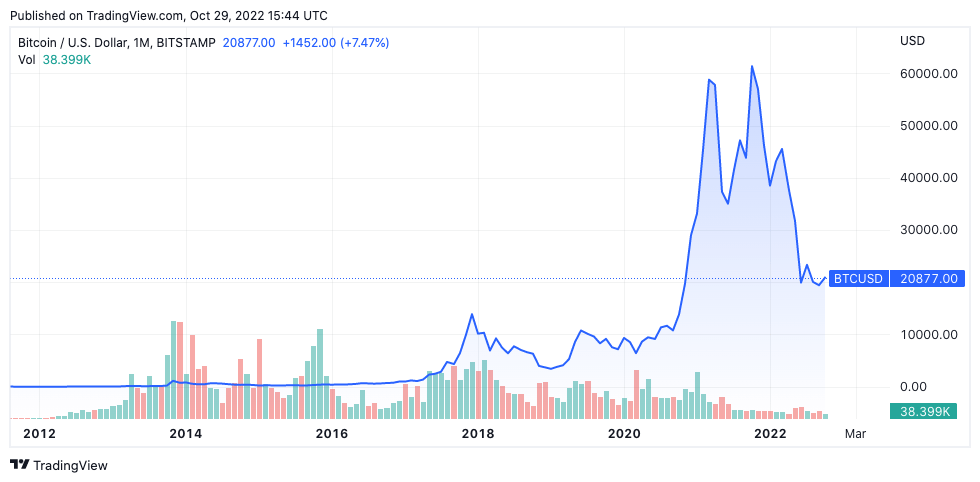

To understand the scope of the crisis, we need to look deep into Bitcoin. Bitcoin is still one of the newest asset classes, but it is one of the most liquid assets in the world.

Over the past year, Bitcoin’s performance has led all other markets.

At the beginning of November 2021, Bitcoin hit an all-time high of $69,000.

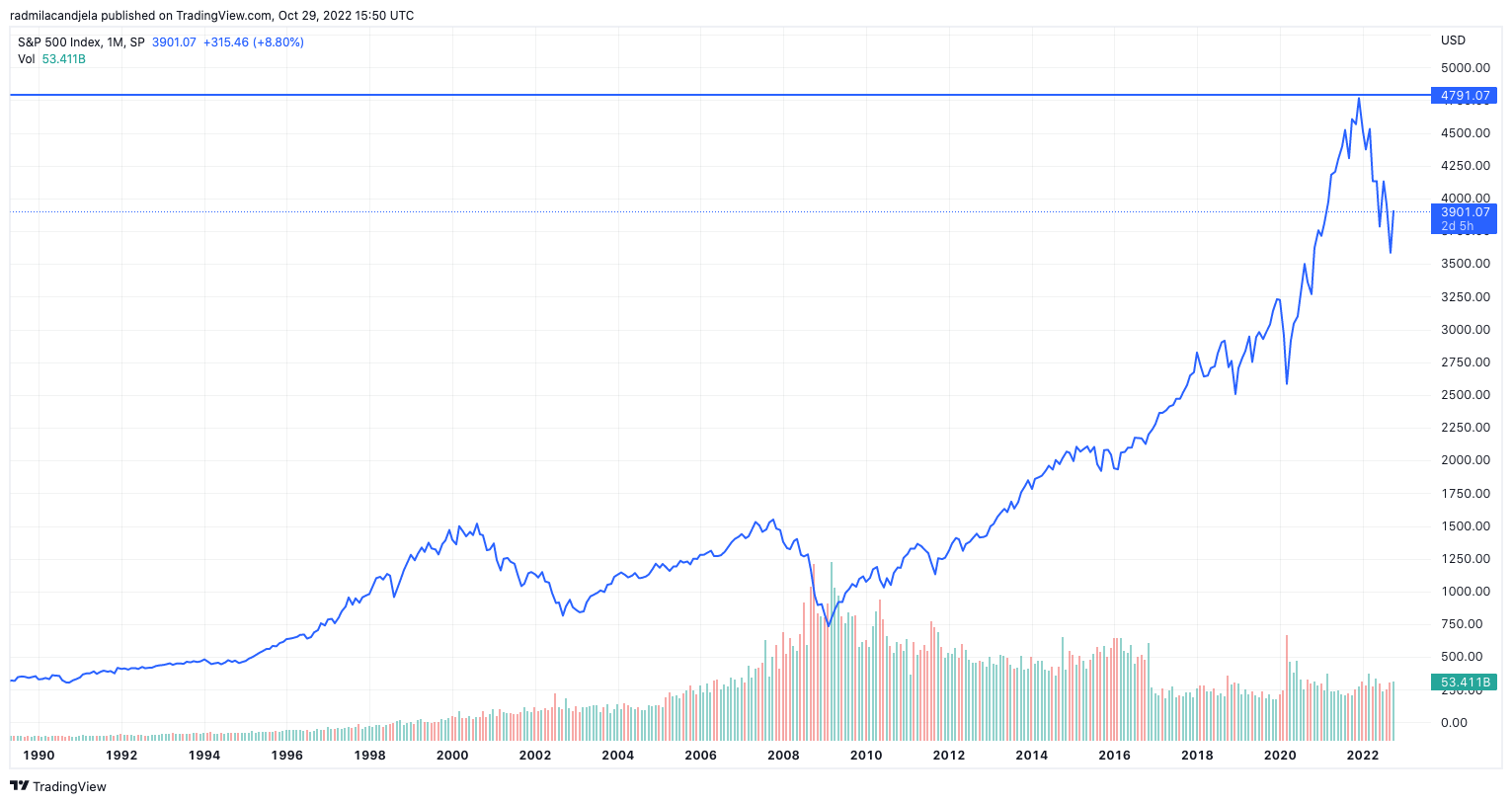

Just two months later, at the end of December 2021, S&P 500 I saw that peak.

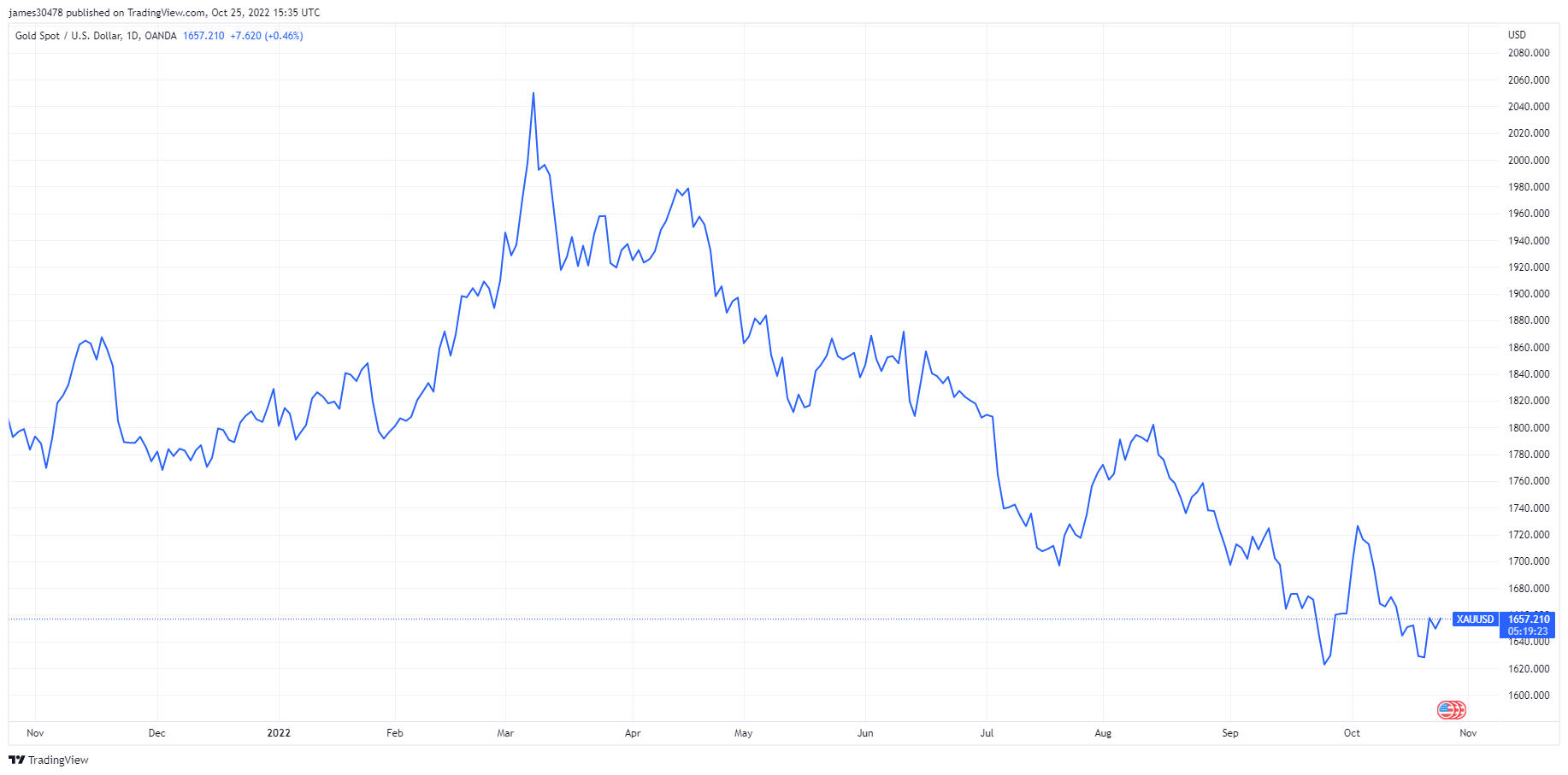

March 2022, Money This was followed by an all-time high.

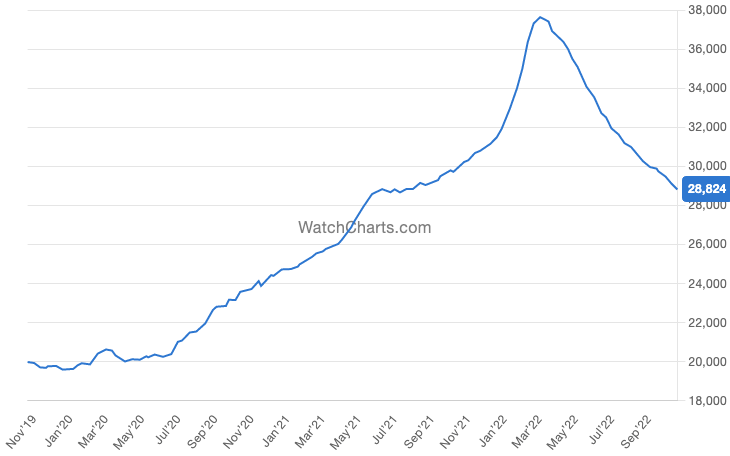

Watches, cars and jewelery also peaked along with gold as the economy’s plentiful capital encouraged people to invest in luxuries and scarce assets. This trend is Rolex Market Indexshows the financial performance of the top 30 Rolex watches on the pre-owned market.

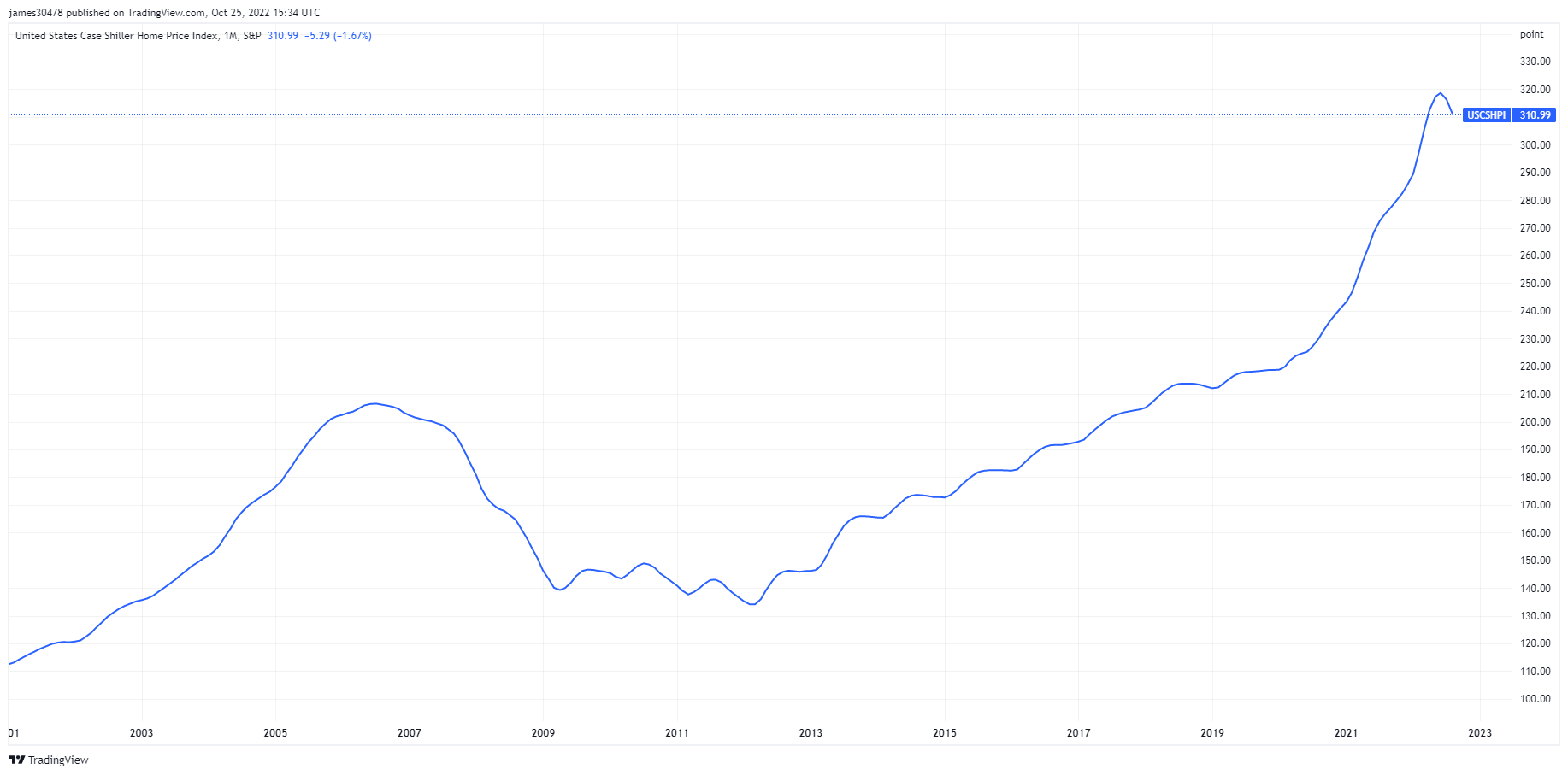

And now, their most illiquid asset, real estate, is about to take a steep decline. The U.S. housing market will peak in September 2022, with the Case-Shiller Home Price Index reaching a record high of 320. Domestic mortgage rates have doubled for him in less than six months due to aggressive rate hikes by the Federal Reserve. Rising mortgage rates, combined with soaring inflation and a sluggish market, are pushing home prices down, wiping billions of dollars out of the real estate market.